Shutterstock

Selecting a real estate agent is one of the most important choices you'll make when buying or selling a home. The decision becomes even more important when you're a veteran or active duty service member looking to use the VA mortgage guaranty. This nearly 70-year-old loan program backed a record 630,000 home loans in fiscal year 2013, nearly double the 2011 volume.

That's a huge increase in just two years' time. You typically only need a credit score[1] of 620 to qualify for a VA loan, which is more than 100 points lower than some other mortgage products. (It's important to check your credit before applying for any home loan, including VA loans. You can pay for a credit score or use a tool like the Credit Report Card[2], which gives you free credit scores and a breakdown of what's impacting your credit.)

As lending standards have become more stringent, greater numbers of veterans are using their VA loan eligibility as the only realistic path to homeownership. The VA loan is a specialized loan program only available to those who have served our country, and, because of this, it comes with some unique requirements. Veterans can really benefit from an agent[3] who can educate and guide them through the entire process.

Closing Costs: If you've done much research on purchasing a home or have purchased a home before, you know there are closing costs associated with the loan. "Closing costs"[4] is an umbrella term for the fees and costs charged by the lender and third parties who conduct work on your file throughout the process, such as a title company. They research the chain of title for the property and complete a significant amount of paperwork to assist in your home purchase. Working with a VA-knowledgeable agent can even save you thousands of dollars when it comes time to go under contract.

The VA has established a list of certain fees[5] that you, as the buyer, are not permitted to pay. This is good for you, because it means your overall cost is lower. But your agent needs to understand these non-allowable costs so they can try to ensure the seller covers them when drafting an offer. Agents should also know how to structure an offer and eventually a contract to deal with closing costs. Because the VA loan is 100 percent financing, meaning you don't have to put any money down, you're not generally able to roll your closing costs into the purchase amount. But that doesn't necessarily mean you're stuck paying them, since your agent can ask that the seller pay all closing costs.

Your second option is to decide how much you want to offer on the home, get an estimate of your closing costs and then add the two together. By making an offer combining the two amounts, you are effectively rolling the costs into the loan. Sellers are generally more accepting of this method because it doesn't change their bottom line.

It's important to note here that the home will have to appraise for the full contract amount. If it doesn't, you'll have to renegotiate to lower the price or walk away from the deal. Agents unfamiliar with this strategy could mean thousands of dollars paid out of pocket to cover these costs or completely restructuring the contract, adding additional time to the process.

Property Requirements: The VA also has a set of minimum property requirements (MPRs) to ensure the property is safe and structurally sound for a veteran homebuyer and their family. A few examples of common MPRs include peeling lead-based paint, exposed wires or lack of a handrail on stairs. These repairs generally have to occur before you can close on the home, and, if the seller refuses or the repair can't be done, you will likely have to walk away from the home.

Failing to satisfy the property requirements can absolutely kill your deal. Veterans can also run into trouble trying to purchase unique properties, like geodesic domes, berm homes, A-frames and other relatively uncommon structures. The home appraisal process[6] revolves around good recent comparable home sales, and it can be tough to find workable "comps" for unusual homes or properties with significant acreage. Appraisals can cost around $500, which is a lot to spend on a home that's never going to fly with the VA appraisal process. That's why agents who understand these requirements can save veterans time, money and heartache.

VA-savvy agents can steer you from problematic properties at the outset, and also help guide you to closing if there's a shot at making the deal work. The experience of a VA-knowledgeable real estate agent is invaluable when shopping for a home. Be sure to ask any agent you interview whether they've closed VA loans before, and, if so, how many. By working with an agent experienced in VA loans, you'll be on the right track to a smooth home purchase.

Source : http://realestate.aol.com/blog/2013/11/21/real-estate-agents-va-loans/

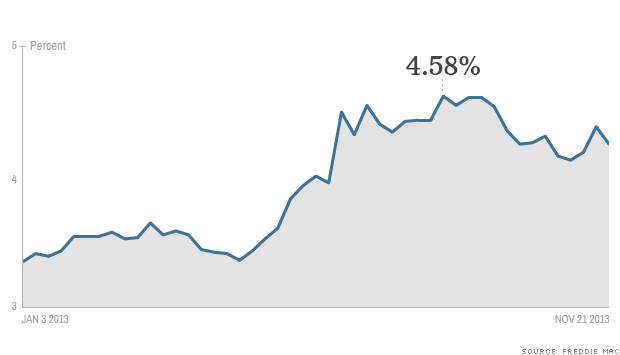

The average rate for a 30-year, fixed-rate loan, the most popular mortgage product, fell to 4.22% from 4.35% last week, Freddie Mac reported. Meanwhile, average rates on 15-year, fixed-rate loans, typically used for refinancing higher interest mortgages, dropped to 3.27% from 3.35% the week before.

The average rate for a 30-year, fixed-rate loan, the most popular mortgage product, fell to 4.22% from 4.35% last week, Freddie Mac reported. Meanwhile, average rates on 15-year, fixed-rate loans, typically used for refinancing higher interest mortgages, dropped to 3.27% from 3.35% the week before.